Accounting

Bookkeeping

Payroll

What Does Gross Wage Include and What Remains Net?

Understand the difference between gross and net salary in the Netherlands. Learn how loonheffing, pension contributions, holiday pay, and DGA salary rules affect what employees actually receive.

•

16 mins

Intro

Dutch payroll is often more complicated than international founders and employees expect. Two people can agree on the exact same gross salary, yet end up with very different net amounts in their bank account depending on pension arrangements, tax credits, company cars, bonuses, or whether they qualify for specific tax schemes. On the employer side, the picture becomes even more confusing. A salary of €3,000 per month rarely costs the employer only €3,000. In practice, total payroll costs are significantly higher once healthcare contributions, disability premiums, pension contributions, and unemployment insurance are added.

The Dutch system is designed around a layered structure of taxes and social security contributions. Some deductions come directly out of the employee’s salary, while others are paid entirely by the employer without reducing the employee’s net wage. That distinction matters. Many employees incorrectly assume every line on the payslip reduces their net income, while many founders underestimate how expensive hiring actually becomes once payroll obligations start. Understanding the full gross-to-net calculation is essential whether you are an employee reviewing your payslip, a DGA determining salary strategy, or a founder hiring staff for the first time.

Brutoloon and Nettoloon: What the Difference Actually Means

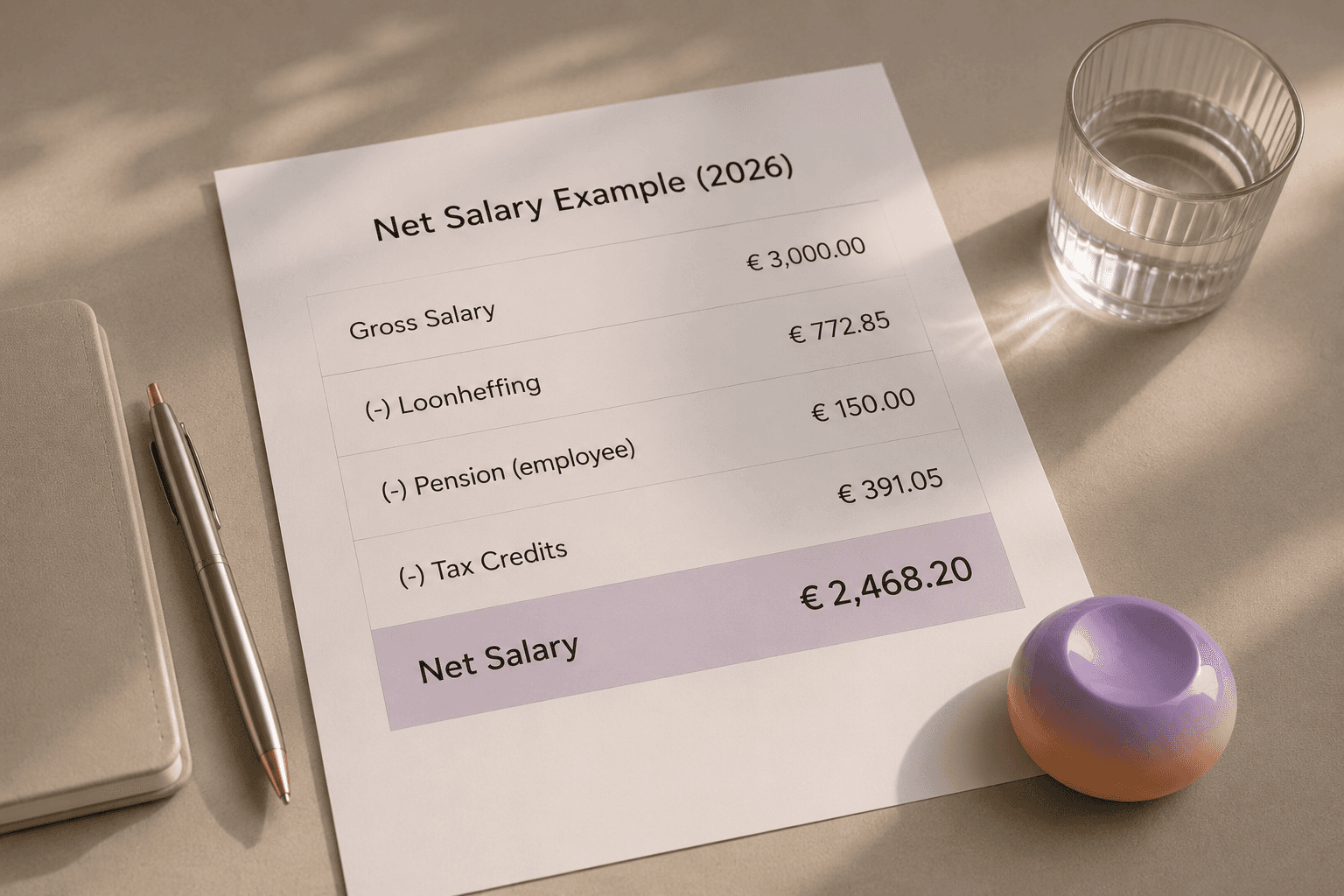

The difference between gross wage and net wage is straightforward in theory but often misunderstood in practice. Gross wage, or brutoloon, is the salary agreed in the employment contract before deductions. Net wage, or nettoloon, is the amount that ultimately reaches the employee’s bank account after payroll taxes and deductions have been applied.

The gap between those two figures is not arbitrary. It consists primarily of Dutch payroll tax withholding, known as loonheffing, and where applicable employee pension contributions. For a standard Dutch employee earning around €3,000 gross per month in 2026, the actual net amount received is usually somewhere between €2,100 and €2,300 depending on pension participation and tax credits.

The taxable basis used for these calculations is the fiscal wage. That figure can differ from the contractual base salary because taxable benefits such as a company car may increase the employee’s taxable income.

Two important clarifications often get missed:

Dutch employees do not personally pay WW or WIA premiums anymore. Since the Wfsv reforms in 2006, those costs sit entirely on the employer side.

The loonheffingskorting reduces payroll tax directly and increases the employee’s net salary. It can only be applied at one employer at a time.

The net salary on the payslip is also not always the employee’s final tax position. The annual Dutch income tax return recalculates the definitive liability. That can lead to either an additional payment or a tax refund after year-end.

What Is Included in Brutoloon?

Gross wage is broader than most people assume. It is not limited to the monthly base salary stated in the employment contract. In Dutch payroll law, brutoloon includes nearly all taxable compensation paid by the employer.

Typical components include:

Base monthly salary

Holiday pay (vakantiegeld)

Thirteenth month payments

Bonuses and commission

Overtime compensation

Taxable allowances

Taxable benefits in kind

Company car bijtelling

Certain employer loans

This means two employees with identical contractual salaries can still have different gross wages on paper. An employee with a company car that triggers bijtelling may end up with a higher taxable gross salary than a colleague without one.

Holiday pay deserves special attention because it is mandatory in the Netherlands. Employers must pay at least 8% of annual gross salary as holiday allowance. Most companies accrue this monthly and pay it out in May. Some collective labour agreements require percentages above the legal minimum.

The thirteenth month is different. It is not legally required but is common in sectors governed by collective labour agreements. Where applicable, it is usually paid in December and taxed as regular salary.

Not every employer-provided benefit becomes part of gross wage. Benefits that qualify under the Dutch werkkostenregeling as gerichte vrijstellingen or designated eindheffingsloon remain outside the employee’s taxable gross wage.

The Dutch Payslip Explained: Every Line Item

A Dutch payslip can look intimidating, especially for internationals seeing terms like loonheffing, Zvw, WGA, and pensioenpremie for the first time. The table below breaks down the most common items and clarifies who actually bears the cost.

Payslip Item | Meaning | Employee or Employer Cost |

Brutoloon | Agreed gross salary before deductions | Employee income |

Vakantiegeld | Holiday pay accrual, minimum 8% | Employee income |

Loonheffing | Payroll tax and national insurance withholding | Employee deduction |

Loonheffingskorting | Tax credit reducing payroll tax | Employee benefit |

Pensioenpremie werknemer | Employee pension contribution | Employee deduction |

Pensioenpremie werkgever | Employer pension contribution | Employer cost |

Zvw werkgeversheffing | Healthcare contribution paid by employer | Employer cost |

Nettoloon | Final amount transferred to employee | Employee receives |

WGA-werknemer | Small disability insurance contribution | Employee deduction |

One of the biggest misconceptions concerns Zvw. Employees often see it referenced on the payslip and assume it is deducted from their salary. For regular employees, that is not how the Dutch system works.

The employer pays the high-rate Zvw contribution of 6.10% in 2026 on top of the employee’s salary, up to the maximum contribution wage of €79,409. It does not reduce the employee’s net salary.

The lower employee-side Zvw contribution of 4.85% applies mainly to DGAs, self-employed entrepreneurs, and benefit recipients.

The WGA-werknemer line is another source of confusion. Unlike WW and WIA premiums, this small differentiated disability contribution may still appear as an employee-side deduction. In practice it is usually well below 0.5% of salary.

How Loonheffing Is Calculated: The Tax Brackets

Loonheffing is the combined withholding tax deducted from employee wages. It consists of two main elements:

Income tax (loonbelasting)

National insurance premiums (premies volksverzekeringen)

The Dutch payroll-specific tax brackets for 2026 are:

Annual Income | Payroll Tax Rate |

Up to €38,441 | 35.82% |

€38,441 to €76,817 | 37.48% |

Above €76,817 | 49.50% |

These are progressive rates. Only the portion of salary above each threshold is taxed at the higher percentage.

The actual amount withheld is reduced by the loonheffingskorting. Two major credits make up this reduction:

Algemene heffingskorting: maximum €3,115

Arbeidskorting: maximum €5,685

Both phase out as income rises.

Employers do not manually calculate these rates each month. Payroll software uses official Belastingdienst withholding tables. Those tables already incorporate tax brackets and credits into the monthly payroll calculation.

Employees working for multiple employers need to be careful. Applying the loonheffingskorting at two jobs simultaneously usually creates an underpayment that must later be corrected through the annual tax return.

For founders and DGAs reviewing their wider tax position, it is worth understanding how much tax you pay across salary, dividends, and corporate profits together.

A Worked Example: Gross to Net at Three Salary Levels

The examples below assume:

Permanent employment contract

Loonheffingskorting applied

No pension contribution

No company car

Standard Dutch payroll situation in 2026

Example 1: Modal Income

Item | Amount |

Gross monthly salary | €3,500 |

Approximate loonheffing | €900 to €950 |

Net monthly salary | €2,550 to €2,650 |

Effective net percentage | 73% to 76% |

This is close to the Dutch modal income range. CPB estimates modal annual income in 2026 at roughly €48,000 gross including holiday pay.

Example 2: Higher Earner

Item | Amount |

Gross monthly salary | €5,500 |

Approximate loonheffing | €1,750 to €1,850 |

Net monthly salary | €3,650 to €3,750 |

Effective net percentage | 66% to 68% |

As salary rises, the percentage reaching the employee’s bank account falls because progressively more income enters the higher brackets.

Example 3: Minimum Wage Level

Item | Amount |

Gross monthly salary | €2,070 |

Approximate loonheffing | Low due to tax credits |

Net monthly salary | €1,700 to €1,800 |

Effective net percentage | 82% to 87% |

At lower salary levels, the combination of tax credits significantly reduces the effective payroll tax burden.

These figures remain indicative only. Exact outcomes depend on pension schemes, CAO rules, company cars, and individual tax circumstances.

What the Employer Actually Pays: Total Loonkosten

Many founders discover too late that gross salary is only part of the actual payroll cost. Employers in the Netherlands pay multiple mandatory contributions on top of the agreed salary.

Employer-side payroll costs in 2026 include:

Employer Contribution | Rate |

Zvw werkgeversheffing | 6.10% |

Awf low premium | 2.74% |

Awf high premium | 7.74% |

Aof small employer | 6.27% |

Aof large employer | 7.63% |

Whk average | Approx. 1.52% |

Wko | 0.50% |

Employer pension contribution | Often 10% to 20% |

The practical result is that total employer payroll costs are usually 25% to 40% higher than the employee’s gross wage.

A practical example:

Item | Amount |

Gross salary | €3,000 |

Employer contributions and premiums | €750 to €1,200 |

Total employer cost | €3,750 to €4,200 |

Flexible contracts are significantly more expensive because they attract the high WW premium of 7.74% instead of the low 2.74% rate for permanent contracts. This is deliberate government policy designed to encourage stable employment.

For many growing companies, payroll administration quickly becomes too technical to handle manually. Working with an accountant or bookkeeper who understands Dutch payroll rules reduces compliance risk considerably.

Holiday Pay, Thirteenth Month, and Bonuses: How They Affect Net

Special payments often create confusion because employees see unusually high withholding in the month the payment is made.

Holiday pay is legally required at a minimum of 8% of annual gross salary. It is usually paid in May and fully taxed as regular income. Because it arrives as a lump sum, employees often feel it is taxed “more heavily” than normal salary. In reality, payroll withholding simply reflects the higher income level for that month, while the annual tax return later settles the definitive amount owed.

The same logic applies to thirteenth month payments and year-end bonuses.

Important practical effects include:

Higher withholding months in May and December

Potential temporary entry into higher payroll brackets

Additional year-end tax adjustments after filing the annual return

Cash flow spikes employers must budget for

For large irregular payments, employers often apply the bijzonder tarief. This special withholding rate attempts to better approximate the employee’s final annual tax position.

Bonuses and commission remain fully taxable income. If a bonus pushes annual income into the top bracket, part of that payment may effectively face the 49.5% marginal rate.

Gross and Net Wage for DGA Directors: How It Works Differently

The gross-to-net calculation for a DGA differs from regular employment in several important ways.

First, the DGA salary must comply with the Dutch gebruikelijkloonregeling. In 2026, the minimum customary salary is €58,000 gross annually, unless a valid lower-salary exception applies.

Second, the healthcare contribution works differently. Regular employees benefit from the employer-paid high Zvw rate, while DGAs fall under the lower 4.85% employee-side contribution structure.

A DGA’s taxable wage includes:

Cash salary

Company car bijtelling

Taxable benefits

Other payroll compensation

The standard loonheffingskorting still applies to DGA salary in the same way it applies to ordinary employees.

The complexity comes from the fact that salary is only part of the personal income picture. Dividend income from the BV is taxed separately in box 2 at 24.5% or 31%.

This creates a two-layer planning structure:

Salary taxation in box 1

Dividend taxation in box 2

Optimizing the balance between the two is one of the most important annual decisions for Dutch founders. The wider strategy is explored in detail in DGA salary vs dividend.

How Gross and Net Wage Affects Hiring Decisions for Dutch Employers

For founders hiring employees for the first time, payroll budgeting mistakes are extremely common.

The most frequent mistake is treating brutoloon as the total cost of employment. In reality, employers need to budget for the full payroll burden including:

Employer social premiums

Pension contributions

Payroll administration

Sick leave exposure

Holiday pay accrual

Insurance obligations

The smarter approach works backwards:

Determine the total employment budget

Subtract employer payroll costs

The remainder becomes the maximum gross salary offer

Net salary also matters competitively. Two employers offering the same gross salary can create very different employee outcomes depending on pension contributions, company car arrangements, or bonus structures.

For founders starting a company in the Netherlands, the administrative burden begins immediately from the first hire. Payroll registration, monthly loonheffingen filings, pension arrangements, and WKR administration all become mandatory obligations.

The choice between a BV or sole trader structure also affects payroll obligations and hiring flexibility significantly.

Employers must also stay compliant with ongoing reporting requirements such as when to file VAT and payroll submissions simultaneously.

Payroll Without the Administrative Headache

Running payroll in the Netherlands is not just about transferring salaries every month. Between loonheffing calculations, pension administration, holiday pay accruals, payroll filings, employment contracts, and DGA salary compliance, payroll quickly becomes one of the most technically demanding parts of running a Dutch BV.

That complexity increases further once your company starts hiring internationally, introduces bonuses, company cars, flexible contracts, or multiple entities. Small payroll mistakes can lead to penalties, retroactive corrections, and unnecessary stress with the Belastingdienst. Most founders simply do not want to spend their time learning payroll legislation instead of building the business itself.

Neno Handles Payroll, Bookkeeping, and Compliance Together

At Neno, we combine AI-driven automation with real Dutch payroll and accounting specialists who actively support growing BVs. From incorporate your BV to ongoing bookkeeping and payroll, everything operates inside one integrated system designed specifically for Dutch entrepreneurs.

That means salaries are processed correctly, payroll taxes are filed on time, holiday pay accruals stay accurate, and your bookkeeping continuously matches your payroll administration in real time. Whether you are paying your first employee or optimising a complex DGA salary structure, Neno helps keep your business compliant while reducing administrative overhead dramatically.

FAQs: Gross and Net Wage in the Netherlands

What is the difference between brutoloon and nettoloon in the Netherlands?

Brutoloon is the gross salary agreed before deductions. Nettoloon is the amount the employee actually receives after payroll taxes and deductions.

How much of my gross salary do I actually receive net in the Netherlands?

For most employees, approximately 65% to 80% of gross salary reaches the bank account depending on income level, pension contributions, and tax credits.

Does the employee pay WW and WIA premiums in the Netherlands?

No. Since 2006, standard WW and WIA premiums are employer-side costs.

What is loonheffing and how is it calculated?

Loonheffing combines payroll tax and national insurance contributions. Employers calculate it using official Belastingdienst payroll tables.

What is the loonheffingskorting and how does it affect my net pay?

It is a payroll tax credit that reduces withholding and increases net salary. It may only be applied at one employer simultaneously.

What is vakantiegeld and how is it taxed?

Vakantiegeld is mandatory holiday pay of at least 8% of annual gross salary. It is taxed as regular income.

Why does my payslip show Zvw if it is an employer cost?

The employer-paid healthcare contribution is often referenced administratively on the payslip even though it does not reduce employee net pay.

How much does an employee actually cost the employer in total?

Usually 25% to 40% more than gross salary once all employer contributions and pension costs are included.

How is the DGA gross-to-net calculation different from a regular employee?

DGAs fall under the customary salary rules and use a different healthcare contribution structure. Their personal income planning also includes dividend taxation.

Can I increase my net pay without increasing my gross salary?

Sometimes. Pension structures, tax-efficient reimbursements, WKR benefits, and salary-versus-dividend optimization for DGAs can all improve effective net income.

Written by

Nick Knuppe

CEO & Founder